Insights

CORSIA: How it works and issues for discussion

Jul 08, 2020The aviation sector accounts for approximately 2% of annual carbon emissions resulting from human activity. Prior to the onset of the global Covid-19 pandemic, passenger numbers were expected to increase to 8.2 billion by 2037 and statistical models predicted that aviation could use up to 27% of the total global carbon allowance if temperature rises were to be limited to 1.5°C by 2050, per the 2015 Paris Agreement. At present, the sector is grappling with the immediate impact of Covid-19, but efforts are still underway to address the long-term environmental impact of aviation, and the Carbon Offsetting and Reduction Scheme for International Aviation (known as “CORSIA”), together with its Standards and Recommended Practices (“SARPs”), represents one of the most important steps in this direction.

Developed by the UN’s International Civil Aviation Organisation (“ICAO”), CORSIA is a global market-based carbon offsetting scheme designed to mitigate CO2 emissions from international civil aviation, by requiring operators to offset any increase in their CO2 emissions above a specific baseline.

What are the key dates and where are we now?

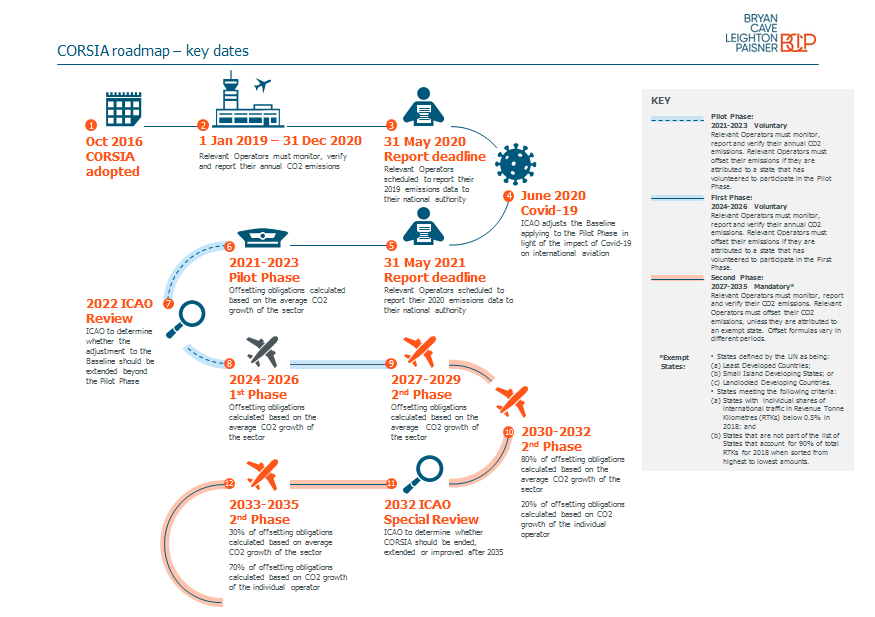

CORSIA operates in a series of Phases, as indicated in the roadmap below (you can select the image to enlarge):

At present, we are in the initial period (1 January 2019 – 31 December 2020) when all civilian operators that emit more than 10,000 tonnes of CO2 per year, operate aeroplanes with a maximum take-off weight of more than 5,700kg and operate a route between two signatory states (each, a “Relevant Operator”) must monitor, report and verify their annual CO2 emissions. Relevant Operators were scheduled to submit their 2019 emissions data to their national authorities by 31 May 2020, and are scheduled to submit their 2020 emissions data to their national authorities by 31 May 2021. The relevant national authorities will then collect this data and submit it to the ICAO through the newly launched CORSIA Central Registry, an online portal designed to facilitate information-sharing between signatory states and the ICAO.

The ICAO will then use this data to calculate the baseline against which all future increases in CO2 emissions must be offset (the “Baseline”). When CORSIA was originally adopted, the Baseline was defined as the average of the total CO2 emissions for 2019 and 2020 on routes covered by CORSIA. However, in light of the impact of Covid-19 on international aviation traffic in 2020 (which would have made the Baseline far lower than originally anticipated) and following lobbying led by IATA, the ICAO announced in June 2020 that the Baseline in respect of the Pilot Phase (2021-2023) will be determined based on the total CO2 emissions for 2019 only. The ICAO is due to revisit this issue in 2022, when it will consider whether, going forward, the Baseline should continue to be based on 2019 emissions data only, or whether it should revert to being calculated based on an average of emissions data from 2019 and 2020.

How does CORSIA work?

Once the initial period ends and the Baseline has been calculated, the Pilot Phase begins. The Pilot Phase and the First Phase are both voluntary in that while Relevant Operators must always monitor, report and verify their CO2 emissions, signatory states can opt into or out of the offsetting regime. By contrast, the offsetting regime is mandatory during the Second Phase (beginning in 2027) for all signatory states other than a few exceptions (although these excepted countries can still choose to participate if they wish). The offsetting regime therefore applies, during the Pilot Phase and the First Phase, to any Relevant Operator attributed to a signatory state that volunteers to take part in the Pilot Phase and/or the First Phase and, during the Second Phase, to any Relevant Operator attributed to a signatory state not falling into one of the Second Phase exceptions (each, a “Participating Operator”).

CORSIA operates on a three-year compliance cycle (the Pilot Phase and First Phase both last three years, and the Second Phase is broken up into three-year sub-phases) and each three-year period operates as follows:

- All Relevant Operators must monitor their annual fuel consumption and produce annual emissions reports.

- These annual emissions reports must be verified by an independent, ISO 14065 accredited third party and are then submitted to the relevant national authorities.

- At the end of each three-year period, ICAO notifies each Participating Operator of its total offsetting obligations relating to that three-year period.

- Participating Operators can discharge their offsetting obligations either by purchasing qualifying emissions units, or by using lower carbon “CORSIA eligible” fuels. Fuels will be considered “CORSIA eligible” if they meet specified sustainability criteria and are certified by an approved sustainability certification scheme.

- Each Participating Operator must then submit a cancellation report to the relevant national authority demonstrating that they have satisfied their offsetting obligations.

Potential Issues

1. Jurisdictional Consistency

Not all states have signed up to CORSIA, and not all signatory states have volunteered to participate in all Phases. The effect of CORSIA also varies from operator to operator because the applicability of CORSIA depends not on the jurisdiction of incorporation or centre of business of an operator, but on the specific routes that it covers. Each signatory state is responsible for implementing and transposing CORSIA and the SARPs into domestic law, meaning that signatory states may impose different legal requirements.

2. Enforceability

The ICAO currently has no legal right to enforce CORSIA or the SARPs against Relevant Operators or any other private entity. Instead, compliance and enforcement (e.g. for failing to purchase enough credits or accurately report emissions) are left to signatory states, and at present the ICAO has not issued any guidance as to what enforcement action states should take.

3. Owner Liability

The SARPs provide that an aircraft owner (as identified in the aircraft registration documentation) could be made liable for a Participating Operator’s failure to sufficiently offset its CO2 emissions. For example, if a signatory state is unable to enforce a Participating Operator’s offsetting obligations because it has become insolvent, the compliance obligations could potentially fall on the aircraft owner.

How might CORSIA affect aircraft financing and leasing documentation?

Operators, aircraft owners and financiers will need to monitor CORSIA’s evolving legislative landscape and consider what documentary measures are appropriate.

A point to note is that the SARPs allow Relevant Operators to request that regulators keep their emissions data confidential, in recognition of the fact that emissions data can provide important commercial intelligence on operators’ fuel use. Therefore, lessors and financiers might consider addressing this issue by requesting that the Relevant Operator in question agree to waive this right, in order to comply with reporting obligations under transaction documentation.

ESG and aviation

When CORSIA was adopted by the ICAO in October 2016, it was hailed as an important milestone both for aviation and for wider environmental progress. Almost 4 years on, more than 85 countries, representing more than 75% of international aviation activity, have volunteered to participate in the Pilot Phase and the First Phase, and between 2020 and 2035, CORSIA is expected to mitigate around 2.5bn tonnes of CO2. Elsewhere, operational improvements such as identifying weight-savings and utilising single-engine taxiing are increasing fuel efficiency and investments are being made in new, less carbon-intensive technology, such as sustainable aviation fuel, as well as in infrastructure improvements, including streamlining routes and noise-dampening airports. Meanwhile, progress is also being made in the finance markets to increase the focus on ESG-positive investments. Clearly, positive steps are being made to meet the aviation industry’s long-term goal of reducing CO2 emissions by 50% by 2050, compared with 2005 levels.

But if international air traffic remains depressed for a number of years to come, as a result of the Covid-19 pandemic’s impact on the aviation industry, it is possible (and maybe likely) that actual emissions will not rise above the Baseline in the immediate future. Consequently, Participating Operators may not be required to offset their emissions at all for a number of years until air traffic levels begin to return to a normal level.

Related Capabilities

-

Finance

-

Transport & Asset Finance

-

Aerospace & Defense